Ans: It ranges from 6% to 10% as per your loan type.

Construction Loan Rates 2026 with Definition, Mechanisms, Types, Factors, Hidden Costs & More!

The construction loan rates, like any other loan rates, are highly dynamic. A lot of economic conditions influence their magnitude. Yet, you can manage to lower your interest rates if you know the trick. That is just a matter of knowing the process well in advance. For example, you can work on improving your credit score, and then it will help you get lower rates for your future construction loan needs. For more such ideas and key information around the construction loans and their rates, follow along.

Table of Contents:

- What are Construction Loan Rates?

- Current Construction Loan Rates in 2026

- How Construction Loan Interest Works?

- Factors That Affect Construction Loan Rates

- Types of Construction Loans and Their Rates

- Construction Loan Rates vs Mortgage Rates

- Average Construction Loan Rates by Credit Score

- Fixed vs Variable Construction Loan Rates

- Construction Loan Rates by Loan Term

- Construction Loan Rates for First-Time Home Builders

- Which One is Right: Bank vs Private Lender Construction Loan Rates?

- How Economic Trends Impact Construction Loan Rates?

- How to Use the Construction Loan Rate Calculator?

- Hidden Costs Associated with Construction Loan Rates

- How to Lower Your Construction Loan Interest Rate?

- Common Mistakes When Comparing Construction Loan Rates

- Construction Loan Rates Last Year in the USA vs Global Markets

- Pros and Cons of Construction Loan Rates

- How to Apply for a Construction Loan?

- Future Trends in Construction Loan Rates

- Conclusion

- FAQs

What are Construction Loan Rates?

Construction loans are for the development of commercial and residential properties. Here, the development includes all the crucial stages of making a building, right from the land purchase to the finished structure, ready to live in or rent out. Construction loans are available for all types of houses, complexes, and other building requirements.

Furthermore, construction loan rates vary from project to project. The higher a house’s structure, the higher the cost of the project will be. And, the higher the rates will ultimately become. The nature of this loan is short-term. No one is provided a construction loan for a very long stretch of time, i.e., 20 or 30 years. And, often, the loan gets converted into a permanent mortgage after the completion of a project.

Current Construction Loan Rates in 2026

The average range for the construction loan rates is between 6% and 8%. However, if your credit isn’t good enough, expect an interest rate of around 10% or even more. Your loan history has a lot to say in the determination of the rate at which the construction loan is disbursed.

Consider the variation in the rate for the different types of construction loans.

| Construction Loan Types | Construction Loan Rates |

| Construction-to-permanent loans | 6% to 7% (for 10 years) |

| Construction-only loans | 5% to 10% |

| Owner-building loans | 6% to 10% |

| Renovation loans | 6% to 10% |

All types of residential construction are eligible for this loan. You just have to have a good credit score with all the proper documents that the lender requires.

How Construction Loan Interest Works?

How the construction loan interest rates work is a dynamic process. To understand its nitty-gritty, you will have to dig deeper. Monthly interest payments vary from one month to another based on the amount drawn from the loan in a given month.

For example, suppose you draw $20,000 of your $2,85,000 construction loan. In that case, your interest rate will apply to the sum of $20,000. Furthermore, if for the next month, you take $50,000 out, then the interest will apply to it. This way, the interest amount you need to pay will differ.

Let’s take an interest rate of 5%. Then, for the $20,000 withdrawal, you will have to pay $1,000 as an interest payment. And, it will turn into $2,500 for a $50,000 withdrawal.

Also Read: Construction Safety Checklist: A Brief Walking Through OSHA-Supported Safety Guidelines!

Factors That Affect Construction Loan Rates

There are several factors that affect the rates of home building loans. They are, namely, credit score, loan amount, down payment, builder reputation, and economic conditions.

- Credit score: The higher the credit score, the lower the interest rate becomes. And, your loan requests also get approved easily.

- Loan amount: A loan approval of $100,000 will have lower rates of interest than that of $200,000. So, the higher the loan size, the higher the interest rate becomes.

- Down payment: That is also a major factor. If you have to pay a large down or initial payment, that means your interest rate will be lower. And, the opposite would mean that you will have to face a higher interest rate!

- Builder reputation: The reputation of the contractor also has a say here.

- Economic conditions: Suppose you don’t have any current source of income to repay the debt. In that case, the lender will decline your offer. To be precise, it is the case when the loan provider is not convinced of your financial well-being to their advantage.

Types of Construction Loans and Their Rates

Have you heard of the one time close construction loan? It is one of several types of construction loans available for building projects. In short, we will explore the major types as mentioned below in the following sections.

- Construction-to-permanent loans

- Stand-alone construction loans

- Owner-builder loans

- Renovation loans

1. Construction-to-Permanent Loans

This is a one-time close construction loan. It transforms into a traditional mortgage once a construction project is done. That means from the point of completion, your repayment schedule each month will cover both interest and principal. It will be like any ordinary mortgage loan.

Rates here: Between 6.8% and 7% approximately

2. Stand-Alone Construction Loans

This type is also known as the two-time-close construction loan. It is specifically provided to build a home. And, you have to repay the entire sum when the construction is complete. Furthermore, there is also the option of starting a mortgage to meet your refinancing needs. But you have to do it as a separate process anew.

Rates here: 5% to 10% for the initial loan, and an interest rate of 6% to 7% for the mortgage after the completion of the project

3. Owner-Builder Loans

This is a loan option that is available to any borrower who also acts in the full capacity of the home builder. Under this option, both the previously discussed types are included. To be precise, it is more available to licensed builders by trade.

Rates here: Between 6% and 10% for most good credit score customers

4. Renovation Loans

You might not always need loans to build new houses. Sometimes, there is only the need to renovate the existing one. That is where the renovation loans come in handy. Furthermore, you might also want to process this finance option if you are planning to buy a run-down house.

Rates here: Between 6% and 7%, for a home equity line of credit, reaching up to 10%

Houseura tip: If your renovation also includes foundation strengthening, don’t forget to thoroughly assess the foundation repair cost first.

Construction Loan Rates vs Mortgage Rates

Consider the major pros and cons of construction loans virginia and traditional mortgage rates. Generally, the following table explores tenure, disbursement, eligibility, and interest rates.

| Differences | Construction loans | Traditional mortgage loans |

| Tenure | Short tenure (typically 12 to 24 months) | Long-term (typically 15 to 30 years) |

| Disbursement | As per the progress in the home construction process | All funds at once to facilitate the purchase of a house |

| Eligibility | Only available for the construction of homes and other types of buildings | Only available for the purchase of fully finished, habitable homes |

| Interest rates | Higher, often due to short tenure | Lower due to long tenure |

Houseura insight: A mortgage is great for buying expensive houses in America, while the construction loans would do well for most economical house structures, such as a rambler house, a Tudor-style house, etc.

Average Construction Loan Rates by Credit Score

If you have a minimum credit score of 720, you are eligible for the construction home loan from American Bank & Trust. Your interest rate will be as low as 4.99%, which is approximately 5%. Other terms and conditions might also apply. The higher the credit scores, the lower the interest rates will be.

Fixed vs Variable Construction Loan Rates

The construction loan rates are mainly of two types, namely fixed and variable. The following table differentiates between the two based on nature, predictability, budgeting ease, and ideal conditions.

| Differences | Fixed Interest Rates | Variable Interest Rates |

| Nature | Remains constant | Fluctuates based on market conditions |

| Predictability | Higher | Lower |

| Budgeting ease | Higher | Lower |

| Ideal conditions | Long-term projects | Short-term projects |

Construction Loan Rates by Loan Term

The majority of people invested in building something opt for the construction-to-permanent option in construction loans. That is why, consider the fluctuations in the construction loan interest rates by loan term provided below.

| Term | Rates |

| 10 years | 5.8% |

| 15 years | 5.9% |

| 20 years | 6% |

| 30 years | 6.6% |

Point to note: If your credit score is excellent, you might even enjoy an interest rate of 5% or below for a 10-year loan tenure. A typical house doesn’t even take this much time for construction with a capable contractor. It is best to learn about the key steps to building a house in advance. A well-educated mind is better at bargaining with authority.

Also Read: Refinishing Timber Floors: Homeowners’ Guide with Key Insights & Complete Overview

Construction Loan Rates for First-Time Home Builders

For first-time home builders, home building loans are available at high rates due to their newness to the financing. Such borrowers often have the lowest credit scores compared to other borrowers with a good history of well-settled loans.

Consider the major challenges faced by first-time home builders who require construction loans.

- Unfamiliar documentation hassle

- Low disbursement amount

- High interest rates

- Escalation of interest rates in the case of unpaid monthly dues

If you are also a first-time builder, the following tips will help you navigate the process effectively.

- Learn about the terms and conditions thoroughly.

- Don’t forget to ask for hidden charges.

- Never rush the process.

- Analyse all the plans carefully before selecting your construction loan type.

- Read about the four major types of construction loans before requesting approval.

Finally, take the advice of someone who has handled the loan process before, if possible.

Do you know?

Construction loans are available for all construction types. It is not like you only have to build a house to avail of this financial facility.

Which One is Right: Bank vs Private Lender Construction Loan Rates?

If you are stuck between these two lender options, you should consider the following table. It helps you explore which of these two will suit your needs better for construction loans, including the one time close construction loan.

| Feature | Private Lender | Traditional Bank Loan |

| Approval speed | Takes a short while (within days) | Takes long (weeks to months) |

| Long term | 6 to 24 months | 5 to 30 years |

| Approval basis | Asset value | Creditworthiness |

| Best for | Real estate investors, bridge loans, and fix-and-flip projects | Homebuyers, long-term investments, and business owners with better economic conditions |

Do you know?

Major technologies in the construction process, such as robotics in construction, ICF construction, MEP in construction, etc., also affect the loan rates. That is because there is a direct relationship between the amount disbursed and the project cost.

How Economic Trends Impact Construction Loan Rates?

The major economic trends that impact the interest rates for construction loans Virginia or any other state are mentioned below. In short, these factors are inflation, interest rate cycles, and housing demand.

- Inflation: The higher the inflation, the higher the construction loan rates will be. There is a direct correlation between these two factors.

- Interest rate cycles: Booms and troughs are two inseparable aspects of the economic cycle. So, to offset the effects of inflation, the government institution or central banking authorities often raise the interest rates. That then results in low demand for investment, and the high prices automatically come down. On the contrary, when the economy is facing low demand, interest rates are forced to go down. That facilitates high purchasing power through loans and demand increases.

- Housing demand: When the housing demand is high, interest rates also reach their highest point. And, in case of low demands, the bankers have to intentionally lower the rates to spur inactive investors into action.

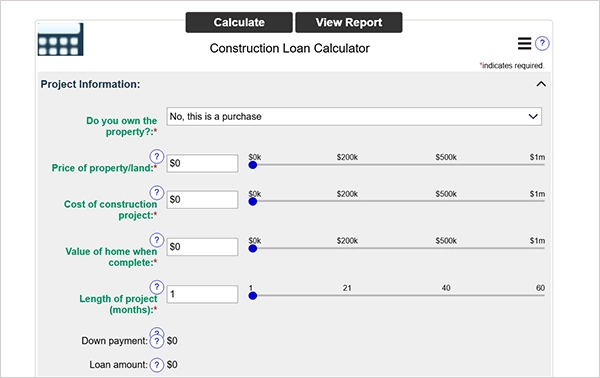

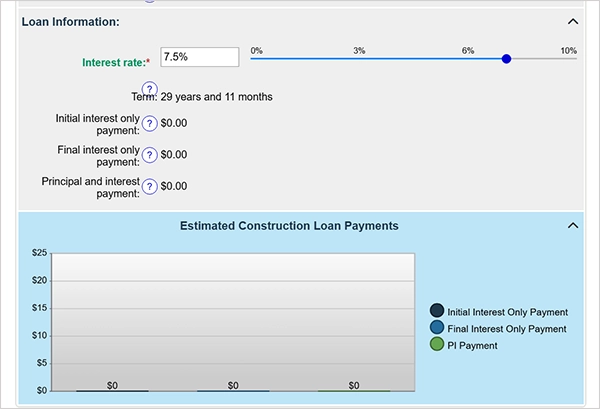

How to Use the Construction Loan Rate Calculator?

The process of using construction home loan calculator depends on the calculator you are using. In other words, it varies from calculator to calculator. If you are using the mortgage calculator, then consider the following elaborations.

With this calculator, you just need to fill out the following sections first on the platform.

Once done, the calculator will automatically offer you the loan details in the format shown below.

Note: Don’t rely on just one calculator while figuring out your loan needs. At least consult two software to cross-check the given details. If possible, also connect with a real provider for quick consultation.

Hidden Costs Associated with Construction Loan Rates

The most common hidden costs in processing construction loans are discussed below. We have covered draw fees, inspection fees, administrative fees, change order fees, interest rate adjustments, and extension fees.

- Draw fees: Each time the funds are withdrawn from the allotted loan pool, a draw fee applies. It is to cover the processing fee related to the withdrawal.

- Inspection fees: Before the approval of each draw, lenders ask for the inspection of the project in construction to make sure that the work has progressed up to the reported extent. Confirming the milestones this way is necessary for reliability. So, such inspection costs also add up to the expenditure chart.

- Administrative fees: Construction loans aren’t disbursed all at once. That is why, before the construction is complete, the lender has to manage the funds. So, a variety of administration fees apply.

- Change order fees: Construction activities are full of fluctuations, twists, and turns. So, when your plans change and you require changes to the original loan terms as well, that culminates in a plethora of additional processing charges.

- Interest rate adjustments: If you need adjustments to be made to the interest rate, you also need to pay extra fees.

- Extension fees: Construction activities aren’t linear. Unexpected things happen and often cause delays to the timeline. So, such delays require extension in the loan tenure, which results in additional charges.

How to Lower Your Construction Loan Interest Rate?

Consider the following tips and see how you can lower the construction loan interest rates. We have curated a quick list for you.

- Work on your credit score: A high credit score means that you can avail of a low interest rate.

- Pay your monthly dues on time: Skipping your periodical dues will drop your credit score. It will affect your prospects negatively.

- Keep a sufficient balance in your bank: So, you won’t have to face a situation where your EMI is missed.

- Reduce the tenure: The lower the tenure, the lower the interest amount that you have to pay over time.

- Moderate the loan size: If you can afford it, only take as little as possible from the bank. The lower the construction loan amount, the lower the interest rates get.

Common Mistakes When Comparing Construction Loan Rates

The major mistakes while comparing the rates among different home building loans are threefold. It includes ignoring fees, not comparing lenders, and misunderstanding loan terms.

- Ignoring fees: Don’t skip a thorough analysis. Hidden charges are often ignored during comparison, and then they later cause unexpected spikes in the repayment amount over the original loan.

- Not comparing lenders: The second problem is that borrowers don’t even compare the services from different providers. That keeps them away from a plethora of services.

- Misunderstanding loan terms: If you don’t understand any part of the policy, make sure that you reach out to the provider. That is essential because misunderstanding can cause major financial losses later.

Construction Loan Rates Last Year in the USA vs Global Markets

There are a variety of construction loan types, including the one time close construction loan. The interest rates also differ from one type to another. Region is another factor that causes fluctuations in the rates of loan interest.

| Nations | Average Rates |

| USA | 7.0% to 9.0% |

| UK/Western Europe | 5.5% to 7.5% |

| Australia | 6.0% to 8.0% |

| China | 4.5% to 6.5% |

| Southeast Asia | 5.0% to 7.5% |

| Africa | 10.0% to 14.0% |

Insights: USA and Africa both have elevated rates, but for completely different reasons. In the USA, this phenomenon is mainly due to inflation-fighting policies. And, in Africa, the credit goes not only to inflation but also to underdeveloped mortgage systems.

Pros and Cons of Construction Loan Rates

No discussion on the rates of construction home loans is complete without the pros and cons. Consider the following table and elaborations in this regard.

| Pros | Cons |

| Flexibility | Higher rates |

| Phased payments | Complexity |

| Interest-only payments | |

| Variety |

Pros

- Flexibility: There are both types of rates involved, namely fixed and variable. So, it ensures the highest flexibility of choice. If you want, you can go with a fixed rate or a variable.

- Phased payments: The payment in a construction loan isn’t disbursed all at once. Instead, it is released in a staged manner. Each time a certain milestone is complete, the borrower has to request a specific amount to be released from the lender’s side.

- Interest-only payments: You only have to pay the interest each month without the principal when the project is under construction.

- Variety: There are a variety of loans available under this category. Four major loan types are construction-to-permanent, stand-alone, owner-builder, and renovation loans. One can choose what serves best.

Cons

- Higher rates: If you don’t have a good credit score, you might even have to deal with an interest rate as high as 10% or even more.

- Complexity: Choosing the stand-alone type of construction loan means you will have to deal with two transactions at the time of project completion. One, you have to close the loan. And second, you will have to start a mortgage. That often increases the complexity of the process for many borrowers.

How to Apply for a Construction Loan?

The process might differ from one provider to another. But the general steps involve preparation, selection, submission, approval, and disbursement.

- Preparation: Find out what essential documents are needed and then arrange for them in advance.

- Selection: Find, compare, and select one of the lenders that suits your needs best.

- Submission: Now, submit your application and wait for the approval.

- Approval: Once the application for a loan is approved, the confirmation of disbursement will be provided.

- Disbursement: As and when required, you can now draw from your funds after the completion of each milestone in your project timeline.

And, not just construction loans Virginia, this process applies alike in institutions across the US states.

Also Read: Commercial HVAC in Fort Worth & Key Considerations Before You Plan Its Installation!

Future Trends in Construction Loan Rates

The construction loan rates are highly volatile. They depend on a variety of factors, such as international trade certainties, national economic certainties, inflation, state policies, etc. Thus, reflecting on the future trends with 100% certainty is a hollow concept. However, as of now, the interest rates aren’t going to spike a lot, given that the construction industry faces a low demand situation for an extended period of time.

Conclusion

Typically, the construction loan rates range from 6% to 10%. However, it mainly depends on the type of loan you are applying for. For example, construction-only loans often have a lower minimum limit, such as 5%. Furthermore, not everyone needs this particular type of loan. Sometimes, you can also manage things with a personal loan. So, don’t forget to assess your needs better before applying for any type of financing product from a lender.

FAQs

Q. What are construction loan interest rates now?

Q. Will interest rates drop to 3% again?

Ans: That isn’t going to be the situation anytime soon.

Q. Do you have to put 20% down on a construction loan?

Ans: It is not mandatory, as it depends on the provider with which you are dealing.