In general terms, the towing company needs commercial auto liability insurance, on-hook towing insurance, garagekeepers insurance, etc.

Towing Company Insurance: What It Covers and Why It Matters!

A small towing business owner was once faced with an instant claim following the experience of a minor roadside accident. The apparently normal employment turned into an economic and legal nightmare. Such a case is typical in the towing business, where unforeseen damages, claims of third parties, or uninsured drivers may pose severe threats. One attack is enough to cut the operations and affect the stability over time without adequate protection.

The towing company insurance is a crucial part of businesses in the towing industry. It helps such firms effectively deal with liabilities arising from the regular operations. This insurance has various aspects, such as on-hook coverage, third-party protection, uninsured/underinsured cases, etc.

Many towing companies struggle with understanding which coverage they truly need, how much protection is enough, and how to safeguard their vehicles, employees, and clients from unforeseen incidents. Rising claims, legal expenses, and property damage risks make it even more challenging for business owners to operate with confidence.

All of these are key considerations that every policyholder needs to think about. Thus, for a detailed elaboration on these topics and choosing the right insurance policy for your towing business, consider the following article.

Table of Contents:

- Why Does Towing Company Insurance Matter?

- What is Towing Company Insurance?

- Why Do Towing Businesses Need Insurance?

- Who Needs Towing Company Insurance?

- What are the Different Types of Towing Company Insurance Coverage?

- What are the Common Risks Faced by Tow Truck Operators?

- How Much Does Towing Company Insurance Cost?

- What Affects the Towing Company Insurance Premiums?

- What are the Benefits of Having Towing Company Insurance?

- How to Choose the Right Towing Insurance Policy?

- Tips to Lower Your Towing Company Insurance Premiums

- Mistakes to Avoid When Buying Tow Truck Insurance

- Final Thoughts

- FAQs

Why Does Towing Company Insurance Matter?

Towing company insurance matters due to the following reasons: protection for customer vehicles (on-hook coverage), third-party liability coverage, protecting assets (physical damage), contractual or legal compliance, and employee safety.

- Protection for customer vehicles (on-hook coverage): If the towed vehicle is damaged or stolen in transit.

- Third-party liability coverage: Against bodily injury or property damage to third parties while towing away a vehicle on duty.

- Protecting assets (physical damage): Coverage for repairs for two trucks that have been involved in accidents, theft, or vandalism.

- Compliance: Many towing companies enter into contracts with municipalities, auto repair shops, and other enterprises before providing services. These contracts often require at least having on-hook towing insurance on the part of the company. Furthermore, legal frameworks of many states also force enterprises to buy such insurance. In addition, having towing business insurance ensures regulatory compliance, strengthens contractual credibility, and protects the company from potential financial and legal risks.

- Employee safety: Protection against liability of the injured staff involved in the accident while working or on duty.

What is Towing Company Insurance?

The towing company insurance is a crucial aspect of businesses in the towing industry. With the help of this insurance, towing companies manage a wide variety of liabilities arising during their day-to-day operations.

In other words, the towing insurance is a form of specialized commercial coverage that financially safeguards the concerned firms by protecting their vehicles, drivers, and the property of others, being towed in the event of accidents.

Towing enterprises engage in towing activities on the road, which is to drag damaged or broken-down vehicles from one place to another. Thus, people in such an enterprise are always highly susceptible to risks, damage, and liabilities, requiring insurance for the least hassle. Having towing business insurance helps minimize financial losses, manage unexpected claims, and ensure smooth day-to-day operations without major disruptions. Many towing companies also collaborate with services like Geico roadside assistance, which further increases the need for proper insurance coverage to handle third-party service requests safely and professionally.

Why Do Towing Businesses Need Insurance?

The major reasons why towing firms need tow truck insurance brokers are, namely, on-hook & cargo liability, liability for third-party property/injury, garagekeepers coverage, physical damage coverage, and workers’ compensation & legal compliance.

- On-hook & cargo liability: Covers damage to a customer’s vehicle while it is being towed or transported.

- Liability for third-party property/injury: Protects the towing company or the insured from lawsuits if a tow truck causes an accident.

- Garagekeepers coverage: Protects customer vehicles from damage, fire, or theft while kept in the care of the insured until collected by the owners.

- Physical damage coverage: Covers the cost of repairing or replacing the towing equipment, vehicles, and tools of the insurance holder after accidents or harmful events.

- Workers’ compensation & legal compliance: Provides coverage for medical expenses and lost wages for employees injured on the job.

Also read: Commercial HVAC in Fort Worth & Key Considerations Before You Plan Its Installation!

Who Needs Towing Company Insurance?

The towing business insurance is required by small towing companies, large towing fleets, roadside assistance providers, and auto repair shops offering towing, as mentioned below.

- Small towing companies: Many small companies can’t meet the big liabilities arising out of their day-to-day operations, thus requiring the assistance of the towing insurance companies.

- Large towing fleets: Giants in the towing industry handle a variety of operations on a daily basis. The higher the number of operations, the more the liabilities to deal with. The biggest construction companies in the US also utilize this form of insurance.

- Roadside assistance providers: Such firms provide services like hauling, jump-starting a battery, delivering fuel, lockdown assistance, installation of spare tires, etc., to the stranded vehicles on the road.

- Auto repair shops offering towing: Some repair service providers also handle towing needs to a certain extent. Thus, they also purchase this coverage to better meet their liabilities.

What are the Different Types of Towing Company Insurance Coverage?

The major types of towing business insurance coverage include commercial auto liability insurance, collision & physical damage coverage, on-hook towing insurance, garagekeepers insurance, medical payments coverage, uninsured & underinsured motorist coverage, and workers’ compensation insurance. These coverages are especially important for towing companies that handle third-party service requests, including partnerships with programs like Geico Roadside Assistance, where proper insurance protection is essential to manage operational and liability risks.

- Commercial Auto Liability Insurance: It covers bodily injury and property damage to others during the towing operation. This commercial auto liability coverage is also typically utilized by major contractors in the construction industry.

- Collision and Physical Damage Coverage: This form of towing insurance pays to repair or replace the tow truck after it has been involved in a roadside collision, theft, fire, or other event.

- On-Hook Towing Insurance: Here, the coverage protects against damage to a customer’s vehicle while it is hooked to the tow truck in transit.

- Garagekeepers Insurance: Garagekeepers towing insurance is available to cover damage to the customer’s vehicles while they are stored in the care of the towing service provider.

- Medical Payments Coverage: This category under the towing insurance concerns itself with providing coverage for medical bills for the insured person during accidents. The person can be either a staff member or the insured themselves.

- Uninsured and Underinsured Motorist Coverage: This special coverage under the commercial tow truck insurance pays for damage from accidents by uninsured and underinsured motorists. Mishaps caused by such unprotected motor vehicle owners are called hit-and-run accidents, as here the information about the accused isn’t available.

- Workers’ Compensation Insurance: When the employee is injured while carrying out a towing operation as part of their job due to a mishap, the company pays for medical bills and lost wages through this part of the coverage.

What are the Common Risks Faced by Tow Truck Operators?

Besides the liabilities managed by the towing company insurance, the towing enterprise has other difficulties to deal with, such as roadside strikes, traffic navigation, loading & securing vehicles, extreme weather conditions, extended hours, and on-site hostility. Companies that work with service providers like usaa roadside assistance must be even more prepared to handle these challenges efficiently while maintaining proper insurance coverage and operational safety standards.

- Roadside strikes: Working on the road, along with other speeding vehicles, automatically puts the towing driver into a highly vulnerable state.

- Traffic navigation: Towing trucks are not small in size. Rather, they are pretty big, yet they have to deal with the tight space and heavy traffic on a daily basis while managing their work.

- Loading & securing vehicles: Sometimes, equipment failure, improper loading, and truck breakdown also lead to a huge nuisance on the spot without successfully towing a vehicle to its desired destination.

- Extreme weather conditions: As the towing businesses are completely road-reliant, facing the extreme weather conditions is an inseparable aspect of work from time to time.

- Extended hours: Long-distance projects often lead to physical and mental fatigue. There are often long hours to drive and manage roadside complications.

- On-site hostility: During on-road accidents, towing drivers also become the immediate subject of the injured and the surrounding people’s hostility.

How Much Does Towing Company Insurance Cost?

The average monthly premium (single truck) of commercial tow truck insurance is approximately $450-$620, which turns into $5,400-$7,440 annually. However, this amount further fluctuates as per the nature of the operation, vehicle type, and driver history.

Taking the cost analysis further, many businesses in the towing industry report that the median cost reaches around $737/month or $8,839/year. And that is true with most commercial auto types of coverage. However, the general liability premium often costs $58/month on average.

What Affects the Towing Company Insurance Premiums?

The following factors affect the towing company insurance premiums, namely experience, claim history, service range, towing business type, fleet size & vehicle types, coverage choices, and safety measures. These elements are carefully evaluated by tow truck insurance companies to determine the level of risk and the overall cost of coverage for a towing business.

- Experience: High experience promises a low premium.

- Claim history: The high rate of involvement in accidents in the past has led to a high premium price in the present.

- Service range: Companies with a large area of operation are more susceptible to roadside risks, and thus, they have to pay a high premium for the insurance.

- Towing business type: The insured that only provides services during the waking hours often pays less in terms of the premium than the one who offers 24/7 services.

- Fleet size & vehicle types: The larger the fleet size and the bigger the vehicles get, the more the premium will become. If you are in the construction business, learning about the various types of construction vehicles might help.

- Coverage choices: The nature of the policy a towing company buys also affects the insurance cost, such as the level of liability, on-hook coverage, selected deductibles, etc.

- Safety measures: Firms that utilize telematics, dashcams, and formal driver training programs often lead to lower insurance costs.

What are the Benefits of Having Towing Company Insurance?

The truck insurance comes with a variety of benefits, such as protection for towed vehicles, third-party liability protection, physical damage coverage for tow trucks, garagekeepers liability, uninsured/underinsured motorist coverage, and medical payments coverage.

- Protection for towed vehicles: Coverage for damage to the vehicle of the customer that is being towed away.

- Third-party liability protection: Coverage for damage to the third party involved in the accident, along with the towed and the towing vehicles.

- Physical damage coverage for tow trucks: Coverage for repair or replacement costs for damage to the tow trucks.

- Garagekeepers’ liability: Coverage for damage to customer vehicles stored at the towing service provider’s facility.

- Uninsured/underinsured motorist coverage: Coverage for hit-and-run cases.

- Medical payments coverage: For medical bills and lost wages for the injured employees on the job.

Also read: Foundation Repair Cost, Typical Range & National Average, Cost-Affecting Factors, & Other Aspects

How to Choose the Right Towing Insurance Policy?

Consider the following four-fold plan to choose the right towing insurance policy. This involves assessment, prioritization, compliance, and comparison with different tow truck insurance companies to ensure you select the most suitable and cost-effective coverage for your business needs.

- Assessment: Recognize and define your specific risks and vehicle types, along with other key requirements, before selecting an insurance policy.

- Prioritization: Carefully see which coverage is more important for you, whether on-hook or garagekeepers. Don’t select without thinking about it deeply.

- Compliance: Never buy a policy without going through the state or federal requirements. Some states might require a higher level of insurance than the ordinary prices.

- Comparison: Once you have selected the policy type that suits your needs best, make sure you compare its costs and benefits with those of other service providers as well to find the best deal available on the market.

Tips to Lower Your Towing Company Insurance Premiums

There is only one core principle that works when it comes to lowering the tow truck insurance premiums. And it is effective risk management. The general rule is that the lower the risk, the lower the premium, and vice versa.

Tips for effective risk management are provided below, namely, safety training programs, maintenance protocols, technology integration, comprehensive coverage review, and emergency response plans.

- Safety training programs: Expert drivers, abundant in skills and training, cause fewer accidents. Thus, in that case, the company will have to pay a lower level of premium.

- Maintenance protocols: Keeping towing vehicles and equipment in good condition is also crucial.

- Technology integration: Tools like GPS tracking and dash cameras enhance the capacities of the vehicles for the good.

- Comprehensive coverage review: Regularly reviewing the insurance policy to rule out the possibility of overpaying for unnecessary services is also crucial.

- Emergency response plans: When you have emergency plans in advance, it means that at the time of accidents, the employees will be well-prepared, leading to better risk management and thus affecting the premium accordingly.

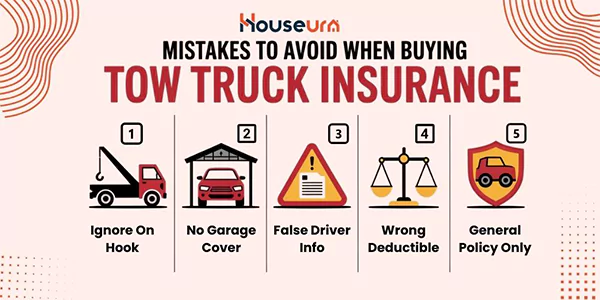

Mistakes to Avoid When Buying Tow Truck Insurance

The following are the top common mistakes that most firms make while buying towing company insurance from tow truck insurance companies, often leading to inadequate coverage, higher premiums, or unexpected claim denials.

- Don’t forget about the on-hook coverage.

- If you store customers’ vehicles at your facility until collected, never neglect the importance of garagekeepers’ liability.

- Many people misrepresent and distort driver records & vehicle info to get an advantage from the side of the insurance company. However, it only leads to the claim rejection later when the truth is revealed from other sources.

- Never choose too high or too low deductibles. Try to strike a perfect balance and choose a middle number for the maximum benefit.

- Go for a specialized insurance for maximum coverage, rather than a low-value general policy.

Final Thoughts

The towing company insurance is the best tool in the hands of businesses in the towing industry to tackle the hectic financial liabilities arising from day-to-day operations. Without this assistance, the company will not only have to deal with the negative effects of the accidents on the revenue but also pay for the damage caused during the job. Thus, tow truck insurance brokers are the best partners with the towing companies to handle a variety of liabilities.

FAQs

What type of insurance does a towing company need?

How much does insurance cost for a tow truck company?

The average monthly premium (single truck) of commercial tow truck insurance is approximately $450-$620.

What insurance do you need to tow?

At least, you need to have insurance for the vehicle. Or, in other words, your towing automobile must be insured.

Is on-hook coverage necessary for towing businesses?

Yes, on-hook coverage is highly recommended because it protects the customer’s vehicle while it is being towed. Without it, any damage occurring during transport may have to be paid out of pocket.

What happens if a towing company does not have proper insurance?

Without proper insurance, a towing company may face legal penalties, contract termination, claim rejections, and heavy financial losses in case of accidents or vehicle damage.